Accounting is Life...

|

Dusting off fake bitches

|

Chapter 15

Corporations: Operations and Additional Shareholders' Equity Transactions

Online Quiz Chapter 15

Online Quiz Answer Chapter 15

Online Quiz Chapter 15

Online Quiz Answer Chapter 15

Reporting the Results of Operations

|

Developing Predictive Information in the Income Statement

psh

|

|

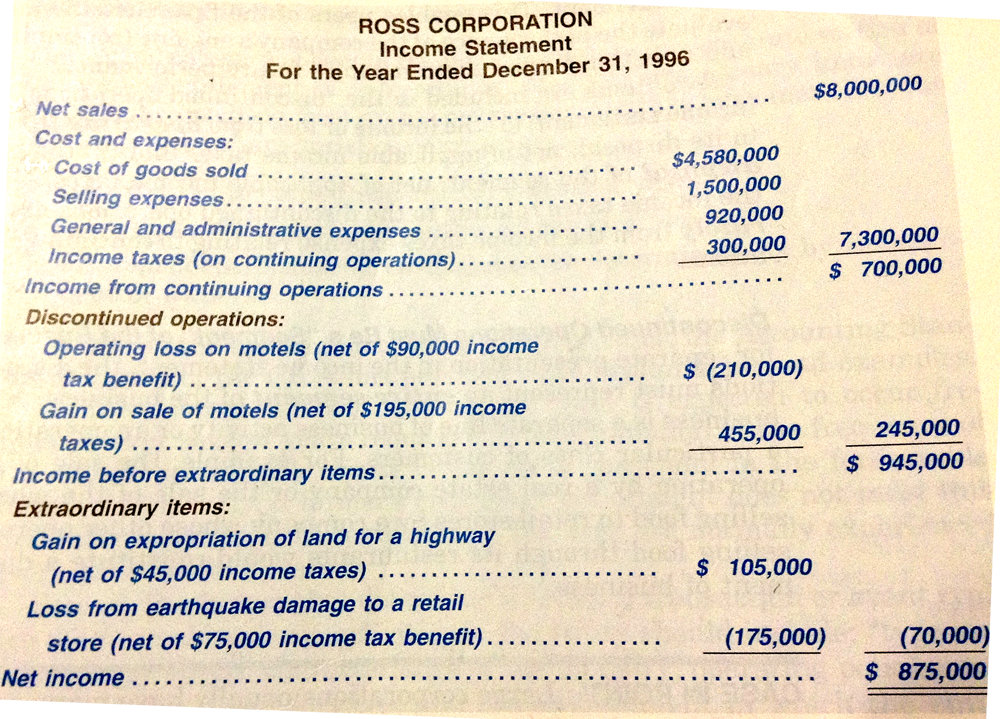

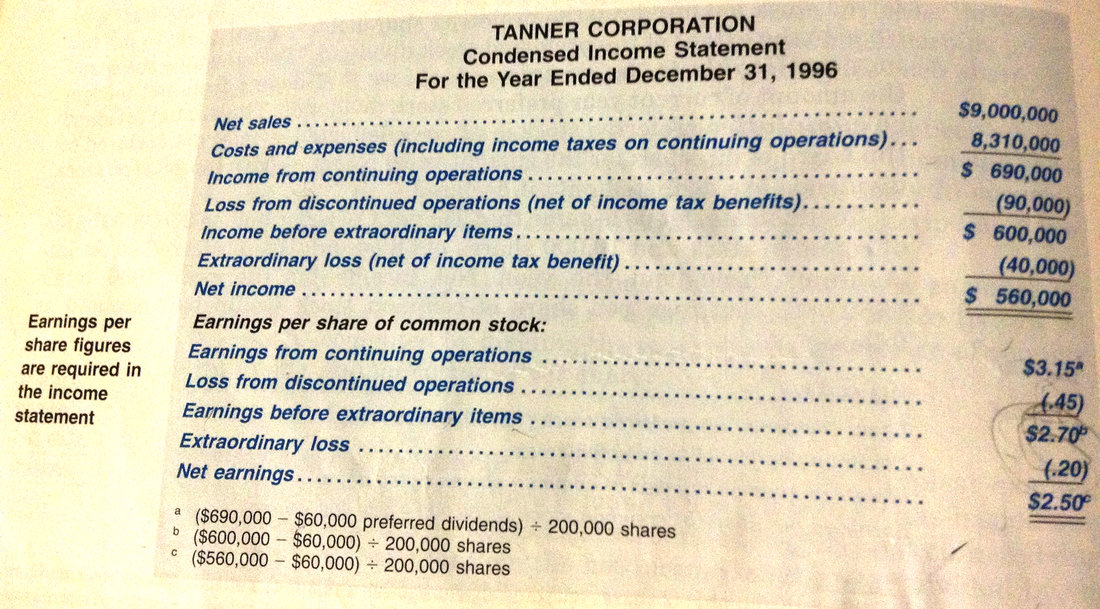

Reporting Unusual Events

Illustration

|

yay...

Accounting Changes

I don't understand

|

Others things that affect the evaluation and prediction of the trend of earnings include

|

bored as fk

Earnings per Share (EPS)

interesting

|

- most widely used statistic

- know earnings per share and the annual dividend per share to decide what to buy EPS = annual net income / average number of common shares outstanding - this concepts applies to common share only - price-earnings ratio (p/e ratio) = market price per share of common stock / annual earnings per share

ACC - 1

|

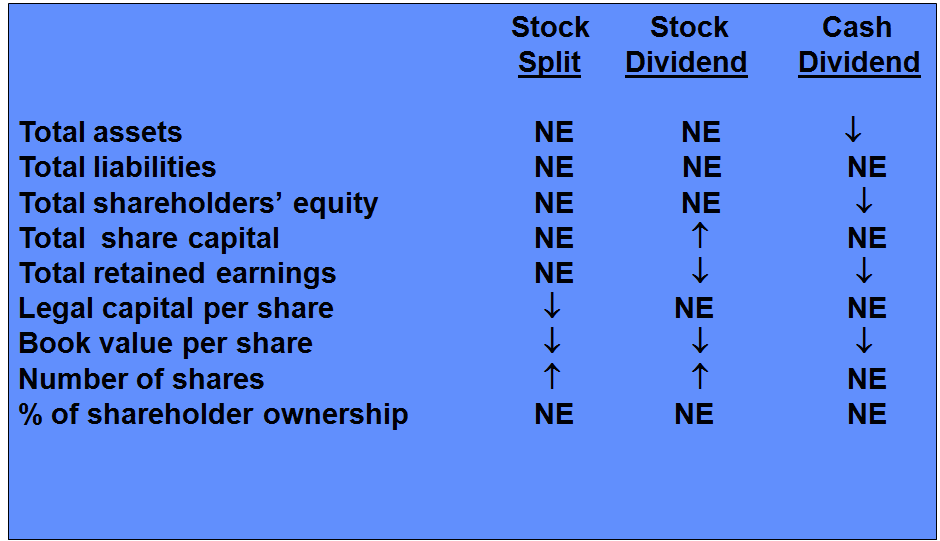

Other Shareholders' Equity Transactions

bored as fk

|

|

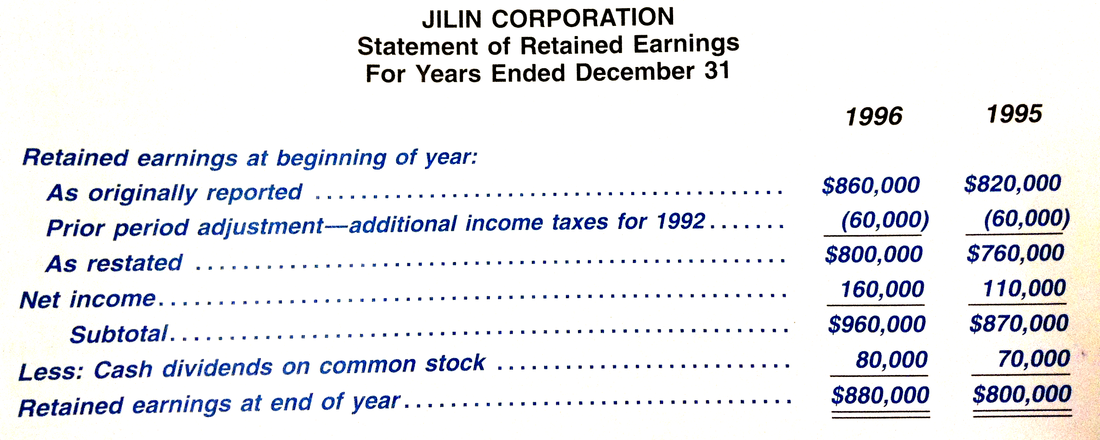

Prior Period Adjustments

idgi

|

A prior period adjustment results from

1. the correction of a material error in reporting net income in previously issued financial statements, or 2. changing an accounting principle. Prior period adjustments are those gains or losses that have all four of the following: 1. are specifically identified with and directly related to the business activities of particular prior periods 2. are not attributable to economic events occurring subsequent to the date of the financial statements for such prior periods 3. depend primarily on decisions by persons other than management or owners 4. could not be reasonably estimated prior to such decisions For examples 1. nonrecurring adjustments or settlements of income taxes 2. settlements of claims resulting from litigation In contrast to extraordinary items, prior period adjustments are excluded from calculation of net income. restatements needed, disclosing: 1. description of adjustment 2. effects on financial statements of current and prior periods. 3. the fact regarding the restatement of the financial statements of prior periods that are presented. - A correction of an error occurs after the books are closed, and relates to a prior accounting period. - A change in an accounting principle occurs when the principle used in the current year is different from the one used in the preceding year

|

Treasury Stock

I don't like this stuff

|

|

Intraperiod Tax Allocation

not even in the textbook

|

|